January 3, 2025 Auto Insurance

Best Auto Insurance Rates: Coverage Without Sacrificing Quality. Finding the best auto insurance rates can feel overwhelming, especially with the wide range of options available. However, by understanding the key factors that influence auto insurance rates, you can make informed decisions and secure a policy that offers the right coverage at an affordable price. This guide will walk you through …

Read More »

January 3, 2025 Auto Insurance

Affordable Auto Insurance Online: Your Car Insurance Premiums. In today’s world, finding affordable auto insurance online can save you time and money. Whether you are a first-time driver or looking to switch your current policy, the internet offers a wide range of options. With the right approach, you can secure an affordable policy without compromising on coverage. This article will …

Read More »

January 3, 2025 Crypto Currency

Predictive Trading Algorithms: Revolutionizing Financial Markets. Predictive trading algorithms are reshaping the financial markets, offering unprecedented opportunities for traders, investors, and financial institutions. By leveraging sophisticated data analysis, machine learning, and artificial intelligence, these algorithms provide powerful insights that enable more informed and efficient trading decisions. What Are Predictive Trading Algorithms? Predictive trading algorithms utilize advanced statistical techniques, machine learning …

Read More »

January 3, 2025 Crypto Currency

Decentralized Autonomous Organizations: Collaboration. Decentralized Autonomous Organizations (DAOs) are reshaping the way individuals and entities collaborate in the digital age. By leveraging blockchain technology, DAOs provide a decentralized and transparent model for governance, allowing stakeholders to make decisions collectively without intermediaries. This article delves into the concept, benefits, challenges, and future prospects of DAOs, offering insights into their transformative potential. …

Read More »

January 2, 2025 Crypto Currency

Wallet Multi-Signature Options: A Comprehensive Guide. In the evolving landscape of cryptocurrency, security remains a top priority for users and businesses. One robust method to enhance digital wallet security is using multi-signature (multi-sig) wallets. This guide delves into the options, benefits, and best practices of wallet multi-signature setups to help you make informed decisions. Understanding Multi-Signature Wallets A multi-signature wallet …

Read More »

January 2, 2025 Crypto Currency

Crypto Legal Compliance: Complex Regulatory Landscape. The rise of cryptocurrency has transformed the financial world, offering unparalleled opportunities for innovation and growth. However, the rapid evolution of this sector has brought about significant regulatory challenges. Understanding and adhering to crypto legal compliance is essential for businesses and investors to operate securely and avoid legal pitfalls. Understanding Crypto Legal Compliance Crypto …

Read More »

January 2, 2025 Crypto Currency

Buy Bitcoin Without ID: A Comprehensive Guide. In the fast-evolving world of cryptocurrencies, anonymity and privacy are often paramount. For many, the ability to buy Bitcoin without ID verification offers both convenience and a safeguard for personal information. This guide delves into the best methods to purchase Bitcoin anonymously, highlighting platforms, strategies, and essential tips to ensure secure and seamless …

Read More »

January 2, 2025 Crypto Currency

Layer-One Blockchain Projects: Blockchain Technology. Layer-one blockchain projects form the backbone of decentralized networks, enabling the secure and efficient processing of transactions. In this article, we explore the intricacies of layer-one blockchains, discuss popular projects, and provide actionable tips and FAQs to deepen your understanding of this crucial blockchain component. What Are Layer-One Blockchain Projects? Layer-one blockchain refers to the …

Read More »

January 1, 2025 Crypto Currency

Wallet Private Key Safety: Protect Your Cryptocurrency Assets. The safety of your wallet’s private key is paramount in the world of cryptocurrency. Losing or exposing your private key can lead to irreversible financial loss. In this article, we’ll explore the essential practices and strategies to keep your private key secure and ensure your cryptocurrency assets remain protected. Understanding the Importance …

Read More »

January 1, 2025 Crypto Currency

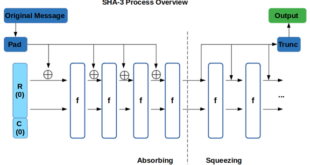

Hashing Algorithms Comparison: Best Option for Your Needs. Hashing algorithms are the backbone of modern data security and integrity. These algorithms play a vital role in applications ranging from password storage to digital signatures and blockchain technology. But with so many options available, how do you choose the right one? This article delves into a detailed comparison of hashing algorithms …

Read More »

January 1, 2025 Crypto Currency

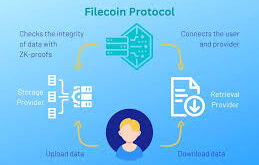

Decentralized Storage Coins: Secure Data Management. In the ever-evolving landscape of blockchain technology, decentralized storage coins have emerged as a powerful solution for secure, efficient, and censorship-resistant data management. As concerns about data privacy grow, these coins offer an alternative to traditional centralized storage systems. This article explores the concept, benefits, and key players in the decentralized storage coin market, …

Read More »

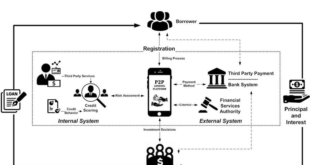

January 1, 2025 Crypto Currency

P2P Lending Platforms: Future of Borrowing and Investing. Peer-to-peer (P2P) lending platforms have revolutionized the way people access loans and invest their money. By eliminating traditional financial intermediaries like banks, these platforms create direct connections between borrowers and lenders. This innovative approach offers attractive benefits such as lower interest rates for borrowers and higher returns for investors. Here’s a comprehensive …

Read More »

December 31, 2024 Crypto Currency

Market Cap Tracker: Market Trends and Investments. Tracking market capitalization (“market cap”) is a critical aspect of understanding financial markets. A market cap tracker offers invaluable tools to monitor the value of companies or cryptocurrencies, helping investors make informed decisions. This article explores the importance of market cap trackers, how they function, and tips for effectively utilizing them. What Is …

Read More »

December 31, 2024 Crypto Currency

Secure NFT Investments: Guide to Safe and Profitable Ventures. The rise of non-fungible tokens (NFTs) has revolutionized the way we perceive digital assets. With the allure of owning unique digital items, NFT investments have become an attractive option for tech-savvy investors. However, navigating this unregulated market can be daunting. This guide aims to provide insights into secure NFT investments, ensuring …

Read More »

December 31, 2024 Crypto Currency

Avalanche Blockchain Overview: A Comprehensive Guide. Avalanche blockchain has emerged as one of the most robust and versatile platforms in the decentralized finance (DeFi) and blockchain ecosystems. Known for its scalability, security, and eco-friendly consensus mechanisms, Avalanche is rapidly gaining traction among developers, investors, and businesses. Introduction to Avalanche Blockchain Avalanche is a decentralized platform that enables the creation of …

Read More »