December 31, 2024 Crypto Currency

Institutional Crypto Investments: The Ultimate Guide for 2024. Institutional crypto investments are reshaping the financial landscape, offering organizations a new frontier for portfolio diversification and growth. As the digital asset market matures, institutions such as hedge funds, family offices, and corporations are exploring opportunities to leverage the potential of cryptocurrencies. This comprehensive guide delves into everything you need to know …

Read More »

December 30, 2024 Crypto Currency

Cryptocurrency Volatility Strategies: Mastering Market Swings. Cryptocurrency markets are infamous for their volatility. From dramatic price surges to sudden dips, navigating this space can be challenging yet rewarding for investors. This article delves into effective cryptocurrency volatility strategies, offering actionable insights for maximizing gains while minimizing risks. Understanding Cryptocurrency Volatility Volatility in cryptocurrency refers to the frequent and substantial price …

Read More »

December 30, 2024 Crypto Currency

Uniswap Liquidity Pools: Understanding and Maximizing Returns. Uniswap liquidity pools have revolutionized the decentralized finance (DeFi) space, offering users a seamless way to trade tokens and earn passive income. Whether you’re a seasoned crypto enthusiast or a beginner, understanding how these pools work is essential to harness their potential fully. What Are Uniswap Liquidity Pools? Uniswap liquidity pools are the …

Read More »

December 30, 2024 Crypto Currency

Wallet Recovery Tips: Safeguard and Retrieve Your Wallet. Losing your wallet can be stressful and overwhelming, but with the right strategies, you can recover it or minimize potential damages. This article provides wallet recovery tips, from preventative measures to steps to take when your wallet goes missing. These practical tips will help you secure your finances and identity, and ensure …

Read More »

December 30, 2024 Crypto Currency

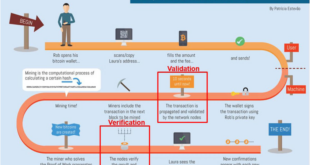

Global Bitcoin Nodes: Their Role and Importance. Bitcoin nodes are an essential part of the cryptocurrency ecosystem, ensuring the security, transparency, and functionality of the Bitcoin network. In this article, we will explore the concept of global Bitcoin nodes, their significance, how they operate, and the benefits they provide. This comprehensive guide will also include tips for setting up a …

Read More »

December 29, 2024 Crypto Currency

Top Crypto Influencers: Leading Voices in Cryptocurrency. Cryptocurrency has taken the world by storm, and in this ever-evolving industry, staying updated is crucial. One of the best ways to navigate the complexities of the crypto market is by following top crypto influencers. These thought leaders share insights, predictions, and tips that can guide both beginners and seasoned investors. In this …

Read More »

December 29, 2024 Crypto Currency

Hybrid Blockchain Solutions: Technology for the Future. In the rapidly evolving landscape of blockchain technology, hybrid blockchain solutions are emerging as a revolutionary bridge between public and private blockchain systems. By combining the best features of both worlds, hybrid blockchains address critical challenges while opening up new opportunities for businesses and developers. This article delves into the core concepts, benefits, …

Read More »

December 28, 2024 Crypto Currency

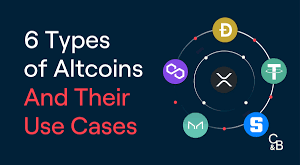

Buy Altcoins Anonymously: A Comprehensive Guide. In today’s digital age, cryptocurrency offers an alternative to traditional finance, providing anonymity and security for transactions. For individuals who prioritize privacy, buying altcoins anonymously is a practical and increasingly popular choice. This article delves deep into how you can achieve this while staying secure and compliant. What Are Altcoins? Altcoins refer to all …

Read More »

December 28, 2024 Crypto Currency

How to Hedge Crypto: A Comprehensive Guide for Investors. Cryptocurrencies are known for their volatility, which can lead to significant gains but also substantial losses. For investors looking to mitigate risks while still participating in the crypto market, hedging is a valuable strategy. This guide will explore how to hedge crypto effectively, providing insights into methods, tools, and practical tips …

Read More »

December 27, 2024 Crypto Currency

Governance Tokens Explained: understanding Role in Crypto In the rapidly evolving world of cryptocurrency, executive tokens have emerged as a vital component of decentralized ecosystems. These tokens not only offer users voting rights but also shape the trajectory of blockchain projects. This article delves deep into the concept of executive tokens, exploring their functions, benefits, risks, and how they differ …

Read More »

December 27, 2024 Crypto Currency

Crypto Yield Farming Guide: Profitable Strategies in 2024. Crypto yield farming has emerged as one of the most lucrative opportunities in the decentralized finance (DeFi) sector. By providing liquidity to decentralized platforms, users can earn rewards in the form of cryptocurrency. However, yield farming is not without risks, and a comprehensive understanding is crucial to maximize profits and mitigate losses. …

Read More »

December 27, 2024 Crypto Currency

Zero-Knowledge Rollups: Scalable Blockchain Technology. Blockchain technology has revolutionized industries by offering decentralized, transparent, and secure systems. However, scalability remains a pressing challenge. Zero-knowledge rollups (ZK-rollups) are emerging as a groundbreaking solution, enabling faster transactions and greater efficiency without compromising security. This article delves into ZK-rollups, exploring their mechanics, benefits, use cases, and potential to transform blockchain ecosystems. What Are …

Read More »

December 27, 2024 Crypto Currency

Cold Storage Wallets: Guide to Secure Your Cryptocurrency. Cryptocurrency investors face various challenges, with security being at the top of the list. Cold storage wallets offer a reliable solution to protect digital assets from cyber threats. In this article, we delve deep into the world of cold storage wallets, their benefits, and how they can safeguard your cryptocurrency investments. What …

Read More »

December 26, 2024 Crypto Currency

AI-Powered Crypto Trading: Revolutionizing Investment Strategies. In the dynamic world of cryptocurrency, staying ahead requires cutting-edge tools and strategies. AI-powered crypto trading is transforming the way traders analyze markets, make decisions, and maximize profits. This article explores the concept, benefits, tools, and best practices of leveraging AI for crypto trading. What is AI-Powered Crypto Trading? AI-powered crypto trading involves using …

Read More »

December 26, 2024 Crypto Currency

Cross-border Crypto Payments: Seamless Global Transactions. Cross-border crypto payments are rapidly transforming the global financial landscape. As cryptocurrencies become increasingly mainstream, their ability to facilitate instant, cost-effective, and secure transactions across borders is gaining significant attention. This guide explores the intricacies of cross-border crypto payments, highlighting their benefits, challenges, and practical tips for seamless transactions. Introduction to Cross-border Crypto Payments …

Read More »